Adobe (ADBE US)

Competition at the edges, dominance at the core

Executive summary

A high-quality software franchise. Adobe’s subscription model, industry-standard products, and asset-light economics have driven ROIC above 30% and ~19% free cash flow CAGR over the last decade.

Losing the low end, defending the fortress. Canva and Figma are winning casual users with simpler, cheaper tools, but Adobe remains deeply embedded in professional workflows where switching costs are high and productivity matters. AI is reinforcing productivity and monetization rather than disrupting the core franchise.

Priced for fear, not fundamentals. After a >50% drawdown, Adobe trades at ~9% forward FCF yield despite a net-cash balance sheet and solid growth rates (10%).

1. Business model

Adobe (ADBE 0.00%↑) operates a subscription-based software business focused on digital creativity, document management, and customer experience solutions. The company generates the vast majority of its revenue from recurring subscriptions, resulting in high revenue visibility, strong cash flow generation, and elevated customer retention.

Like most mature software businesses, Adobe’s model is highly scalable and asset-light. Once software development costs are incurred, the incremental cost of serving additional users is low, leading to structurally high gross margins and strong free cash flow conversion. In our opinion, growth is primarily driven by customer expansion rather than pure user acquisition, as Adobe moves customers from individual plans to teams and enterprise subscriptions, introduces higher-value features, integrates AI capabilities, and monetizes premium tiers.

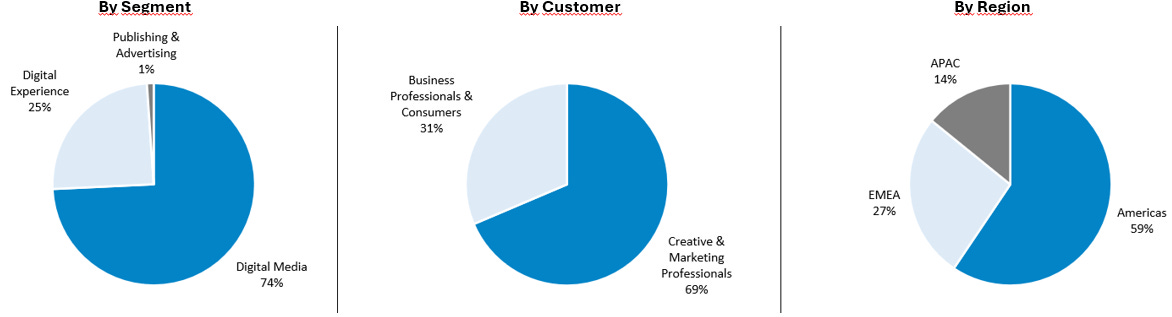

Adobe’s operations are organized into two core segments:

Digital Media (74% of sales): Digital Media encompasses solutions for creating, editing, and managing digital content and documents.

Acrobat is Adobe’s document platform centered on the PDF standard. It enables users to create, edit, sign, and manage documents digitally and is widely used by enterprises for contracts, compliance, and approvals, as well as by consumers for everyday document tasks.

Adobe Express targets non-designers and small businesses, offering fast, template-based tools for creating social media content, presentations, flyers, and short-form videos without requiring professional design skills.

Creative Cloud is Adobe’s flagship suite of professional creative tools and represents the core of the company’s economic moat. These applications are industry standards for designers, photographers, and video professionals, and include Photoshop (image editing), Illustrator (vector graphics), Lightroom (photo management), Premiere Pro (video editing), and After Effects (motion graphics and visual effects).

Higher-tier Creative Cloud subscriptions incorporate AI-driven functionality powered by Adobe Firefly. Firefly enables generative image creation, text effects, and design automation directly within Adobe’s applications, improving productivity and expanding monetization opportunities without displacing professional workflows.

Digital Experience (25% of sales): Digital Experience focuses on helping enterprises manage customer data, personalize content, and execute digital marketing campaigns.

At its core is Adobe Experience Platform, which aggregates customer data from multiple sources—including websites, applications, email, and transactions—into a unified data layer. Built on top of this platform are applications such as Real-Time Customer Data Platform, Customer Journey Analytics, Experience Manager Sites, Adobe Commerce, Journey Optimizer, and Marketo Engage. Together, these tools allow enterprises to design, deliver, and optimize personalized customer experiences across channels.

While strategically important, this segment is more cyclical and competitive than Digital Media

2. Company history & ownership

2.1. Brief company history

Adobe was founded in 1982 by John Warnock and Charles Geschke, initially focused on digital publishing and printing technologies. Its first major breakthrough was PostScript, a page description language that became the industry standard for professional printing and laid the foundation for Adobe’s influence in digital documents. In the early 1990s, Adobe introduced the PDF format and Acrobat, which became a universal standard for document sharing across platforms.

During the late 1990s and 2000s, Adobe expanded into creative software through acquisitions and internal development, forming what became Creative Suite, including Photoshop, Illustrator, and InDesign. These products established Adobe as the dominant software provider for creative professionals.

A pivotal strategic shift occurred between 2011 and 2013, when Adobe transitioned from perpetual software licenses to a subscription-based model with Creative Cloud. The move initially faced customer resistance but ultimately transformed Adobe into a recurring-revenue, high-margin business.

Over the following decade, Adobe broadened its scope from content creation to digital marketing and customer experience through acquisitions such as Omniture, Marketo, and Magento. More recently, Adobe has embedded artificial intelligence across its products via Adobe Sensei and Firefly, reinforcing its role as the core platform for digital content creation and management.

2.2. Ownership

Adobe has no controlling shareholder and is fully free-float.

3. Industry analysis

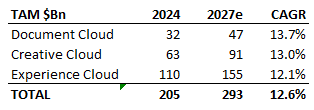

As individuals consume more content, the creativity industry continues to growth. Adobe expects its Total Adressable Market (TAM) to grow at 12-13% CAGR until 20271.

Adobe operates across multiple markets, including creative software, document management, and enterprise marketing solutions. Key competitors include Figma and Canva in creative design, Salesforce and Oracle in customer experience software, and Microsoft and Google in analytics and productivity tools.

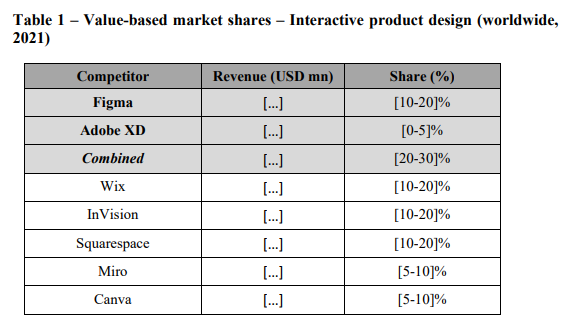

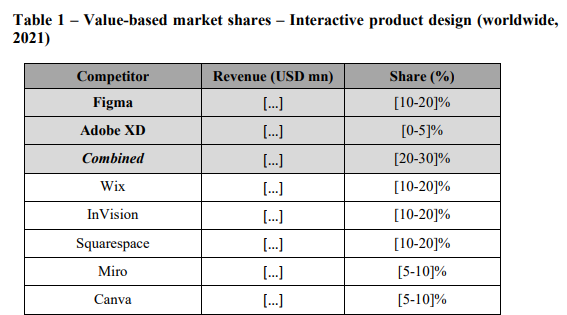

Given that Adobe derives most of its value from Creative Cloud, we focus on competitive dynamics in creative software:

Figma (FIG 0.00%↑): In december 2023, Adobe and Figma jointly abandoned their proposed merge after fifteen months into the regulatory review process2. After reviewing the Statement of Objections from the EC3, it became clear that Figma’s UI/UX (user experience) design product was viewed as superior to Adobe XD and had already begun substituting it. Adobe XD would, in fact, have been discontinued had the transaction been approved.

In addition, the European Commission stated that Figma was highly likely to expand into vector-based design tools (e.g. Photoshop), which would have materially reduced competition in adjacent creative software markets. This potential for future competitive overlap was a key factor behind the transaction’s rejection.

Source: EC Case M.11033 – ADOBE / FIGMA Figma has grown rapidly and taken market share due to its browser-based architecture, real-time collaboration, and ease of use. As a result, Figma should be considered a legitimate competitive threat within design workflows. However, it remains uncertain whether the company can meaningfully penetrate Adobe’s high-end professional customer base, where users rely on a broad, integrated suite of advanced creative tools rather than a single application4.

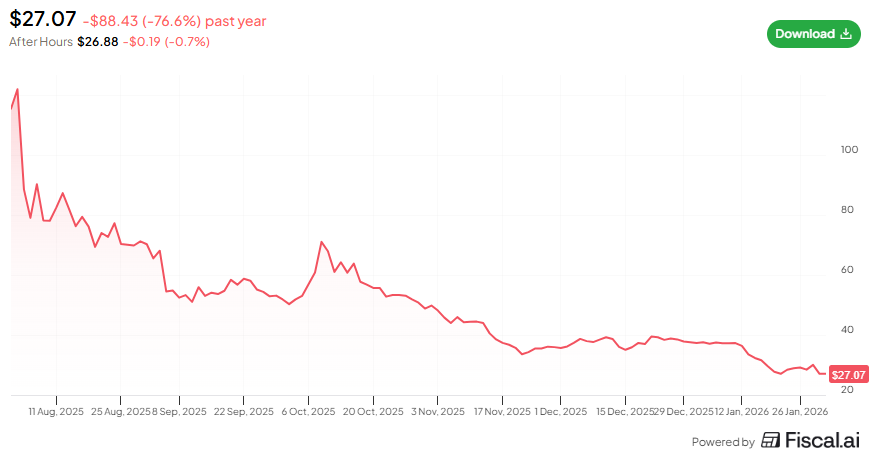

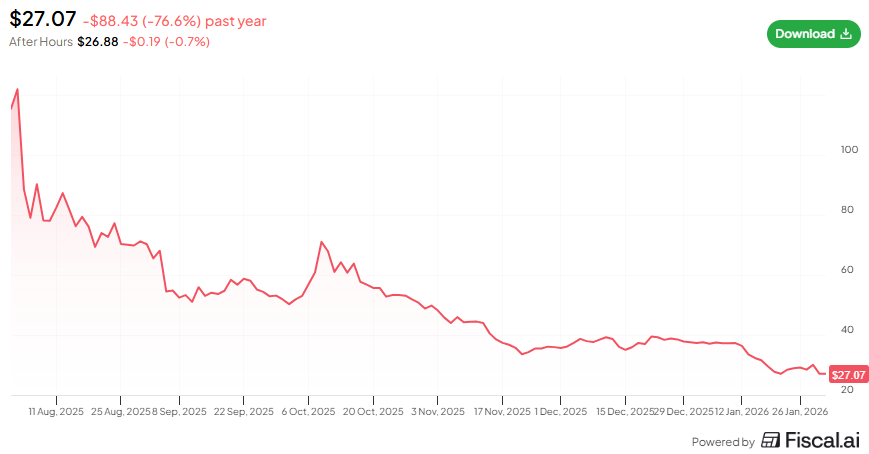

As a side note, while Figma’s top-line growth has been strong, its financial profile has deteriorated. Gross margins have declined, and the company remains unprofitable when stock-based compensation is included, which has been reflected in recent share price performance.

Figma’s stock quote:

Canva is a cloud-based design platform optimized for simplicity, speed, and scale. It targets non-designers and small teams, offering “good enough” creative output through templates and drag-and-drop tools.

In March 2024, Canva acquired Affinity (formerly owned by Serif), a suite of professional design tools with approximately 3 million users. Affinity’s perpetual-license pricing was highly competitive5 relative to Adobe’s subscription model, and its inclusion within Canva’s offering meaningfully strengthens Canva’s positioning.

Canva follows a freemium model, with paid team plans priced well below Adobe’s professional offerings, making it a strong competitor at the low end of the creative stack.

4. Competitive advantage (moat)

Adobe’s products are embedded deeply into professional and enterprise workflows, creating high switching costs and durable pricing power.

Industries use Adobe because it has become the default infrastructure for digital content and documents, not just a set of tools.

Adobe products are industry standards. File formats like PDF, PSD, AI, and INDD are universally recognized and compatible across companies, agencies, printers, and platforms. Using Adobe reduces friction when files move between teams, partners, and clients, which is critical in professional environments. For example, competitors like Figma use different file extensions (.fig). While there are specialized plugins that convert files, this is often inconvenient (disrupts the workflow) and can cause errors.

Adobe tools are deeply embedded in professional workflows. Designers, marketers, video editors, and document teams are trained on Adobe from early in their careers. Switching away would require retraining staff, changing processes, and risking compatibility issues, creating very high switching costs. For example, the Royal College of Arts (one of the most prestigious colleges in design in the world) teaches Adobe’s tools6.

Source: Royal College of Art (RCA) Adobe combines quality, reliability, and scale. Its software handles complex, high-value work—large files, color accuracy, advanced editing, compliance-heavy documents—that lighter or cheaper alternatives often struggle with. For enterprises, reliability and precision matter more than marginal cost savings.

Adobe offers an end-to-end ecosystem. Companies can create content (Creative Cloud), manage documents and approvals (Acrobat), store and organize assets, personalize content, run campaigns, and measure performance (Digital Experience). Few competitors cover the full lifecycle from creation to monetization.

The impact of new competition

Competition from Canva and Figma has clearly weakened Adobe’s position at the low end of the market. These platforms offer simpler interfaces and lower prices, making them attractive to casual users and small teams. However, Adobe remains the most comprehensive solution for professional users who spend full workdays within creative software and require frictionless, high-performance workflows.

We do not expect widespread migration of high-end customers to these alternatives, though continued pricing pressure could accelerate share loss among entry-level users. We are of the opinion that the growth of these new competitors is coming from new users rather than widespread migration from Adobe’s users.

At the entry level, Adobe introduced Adobe Express as a lightweight, template-driven product targeted at casual users, small businesses, and non-professional creators. Express lowers the barrier to entry into Adobe’s ecosystem and allows the company to compete for mindshare among new users without diluting the premium positioning of Creative Cloud. Importantly, Express is designed as an on-ramp rather than a replacement, with seamless interoperability with Photoshop, Illustrator, and other flagship applications.

The impact of AI

Market concerns that generative AI could render Adobe’s tools obsolete appear overstated. While AI models are increasingly effective at performing isolated, low-complexity tasks—such as background removal or basic image generation—professional creative work requires precision, control, repeatability, and integration into complex, multi-step workflows. These are areas where standalone AI tools remain structurally limited.

Professional users do not simply seek visually acceptable output; they require granular control over layers, masks, color management, typography, compositing, and versioning within repeatable production pipelines. In this context, AI is more likely to augment professional workflows than replace them, acting as a productivity lever for automating repetitive, low-value tasks rather than substituting high-value creative judgment.

From an economic perspective, AI adoption may reduce the time spent on routine tasks and, in some cases, the number of personnel required for specific workflows. However, this does not necessarily translate into a proportional reduction in software demand. Instead, it increases the value of professional tools by allowing users to allocate a greater share of their time to higher-value activities. As a result, AI is more likely to reinforce Adobe’s relevance among professional users than undermine it.

Adobe’s strategic response has been to embed AI capabilities directly across its product suite, positioning AI as a feature rather than a standalone product. The company complements its proprietary models with customized and third-party models (including Gemini 3, FLUX, and Luma AI Ray), ensuring flexibility while maintaining workflow integration and enterprise-grade reliability.

Adobe is the leader in the AI creative applications category. Our AI-influenced7 ARR has now surpassed $5 billion, up from over $3.5 billion exiting fiscal year 2024 and we've already surpassed our full year AI-first ending ARR target

Adobe’s CEO - 3Q2025 Earnings Call

Overall, while AI intensifies competition at the low end of the creative market, it is more likely to represent a net opportunity for Adobe’s core professional franchise, strengthening user productivity, supporting premium pricing, and deepening platform lock-in rather than rendering the company’s tools obsolete.

5. Financials

5.1. Growth & profitability:

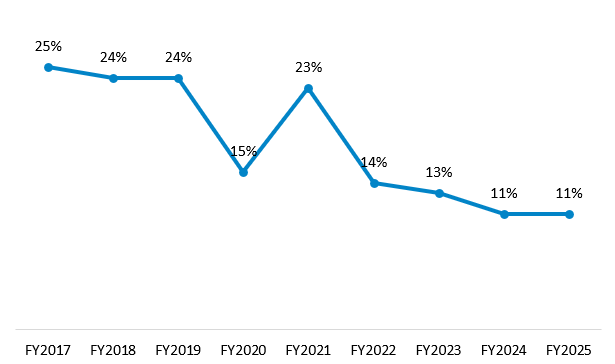

Adobe’s revenue growth has decelerated over the past decade and stabilized around 10%, reflecting both business maturity and increased competition. However, operating margins have expanded significantly as the subscription model scaled, rising from 25.5% to approximately 36.6%.

Sales growth rate (at constant currency since FY2022):

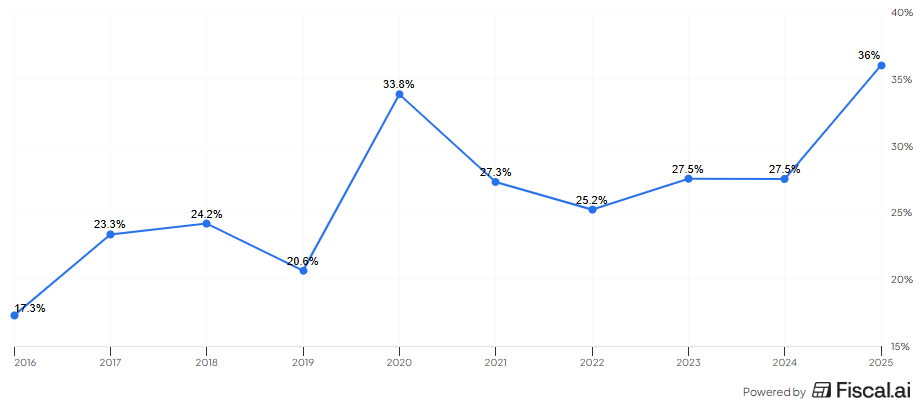

This operating leverage has translated into strong returns on invested capital, consistent with an asset-light software model.

ROIC evolution:

5.2. Cash Flow generation and capital allocation:

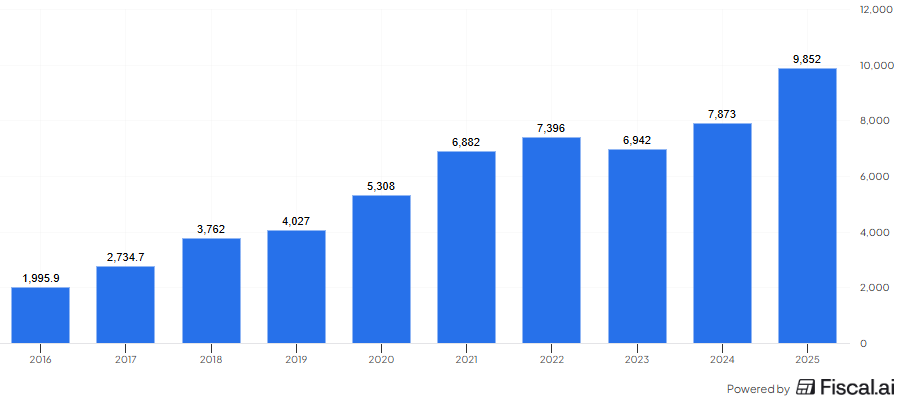

Over the past decade, Adobe’s free cash flow has grown at a CAGR of approximately 19%, an exceptional outcome for a company of its size.

FCF evolution:

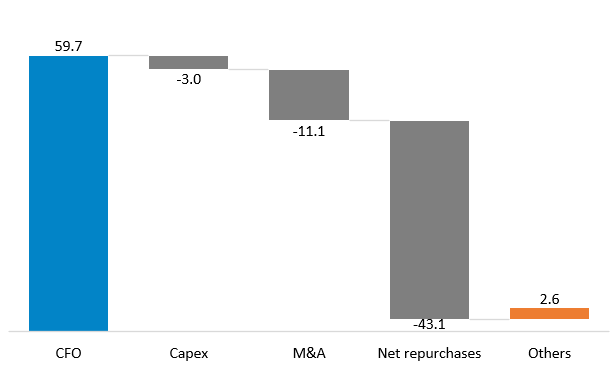

Cumulatively, Adobe has generated nearly $60 billion in operating cash flow since FY2016, of which approximately $43 billion (72%) has been returned to shareholders via share repurchases.

Cumulative Cash Flows (FY16-25):

5.3. Balance sheet and financial risk:

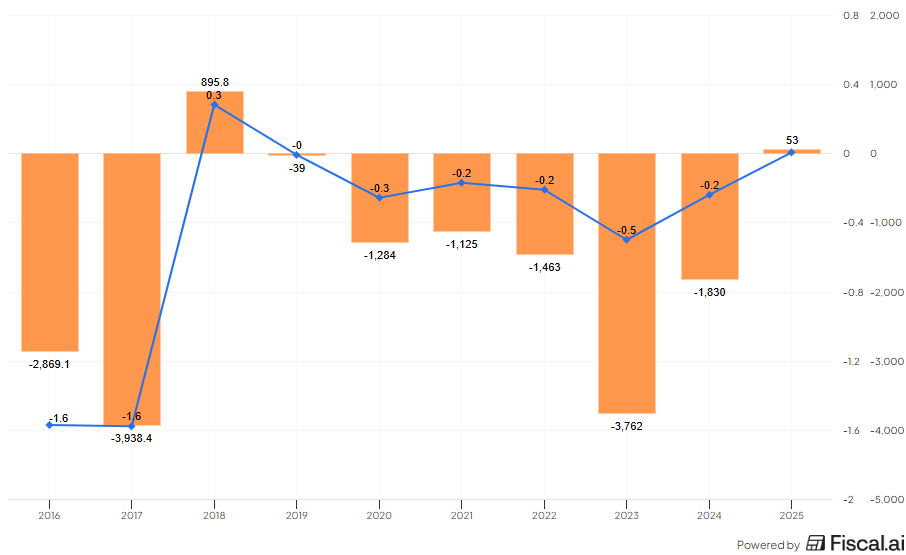

Adobe maintains an exceptionally strong balance sheet with no material net debt and substantial financial flexibility.

Evolution of Net Debt (orange) and ND/EBITDA (blue):

6. Valuation

Share price has declined by more than 50% over the past two years, driven by concerns around AI disruption and increased competition. While these risks are real, current valuation levels appear to reflect an overly pessimistic scenario.

At approximately a 9% forward free cash flow yield (as per Fiscal.ai figures), Adobe trades well below its historical valuation range despite maintaining strong margins, cash flow generation, and competitive positioning.

Adobe’s forward FCF yield over the last 10 years:

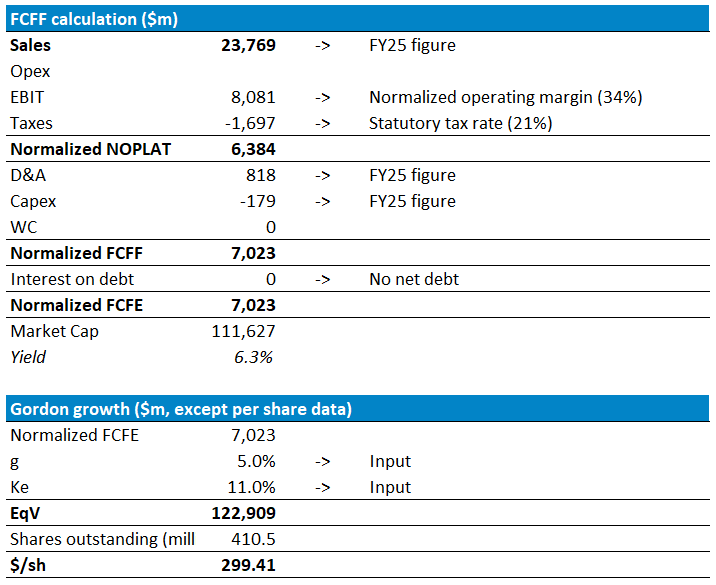

We derive our valuation using a normalized free cash flow to equity (FCFE) framework. Based on FY25 financials and normalized operating assumptions, we estimate that Adobe can sustainably generate approximately $7 billion in FCFE, with long-term growth of 5% per annum.

While this growth assumption may appear optimistic at first glance, it is reasonable when viewed in the context of the current macro environment. With inflation running at approximately 2.7% and the U.S. 10-year Treasury yield at around 4.2%, our growth assumption effectively implies a 200 basis point real growth premium for a company that continues to grow revenues at roughly 10% per annum. We therefore view this assumption as balanced rather than aggressive.

On the discount rate, we apply a cost of equity of 11%, incorporating a 100 basis point risk premium to reflect uncertainties related to generative AI disruption and intensifying competition, particularly at the lower end of the creative software market. Given Adobe’s business quality (ROIC >30%), balance sheet strength, and cash flow durability, this assumption could ultimately prove conservative; however, we prefer to err on the side of prudence.

Under these assumptions, our Gordon Growth valuation implies an equity value of approximately $123 billion, equivalent to $299 per share. At current market prices, this suggests that much of the perceived AI and competitive risk is already reflected in the valuation.

Disclaimer

As a reader of Black Tower Capital, you agree with our disclaimer. You can read the full disclaimer here.

https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/amju76er354.pdf

https://www.figma.com/blog/figma-adobe-abandon-proposed-merger/

https://ec.europa.eu/commission/presscorner/detail/en/ip_23_5778

https://altersquare.medium.com/competing-on-usability-not-features-lessons-from-figma-vs-adobe-940f2e229682

Affinity Publisher is similar to Adobe InDesign, Affinity Photo is similar to Adobe Photoshop, and Affinity Designer is similar to Adobe Illustrator.

https://www.rca.ac.uk/study/the-rca-experience/living-costs/

Our understanding of “AI influenced revenue” is the revenue generated by customers that moved to a higher service level that offers AI and nothing else more. AI-only revenue stands at $125MM ARR as of 1Q25.

https://companycharts.substack.com/p/why-adobe-is-the-best-value-pick?r=6kpr46