Doximity (DOCS US)

The "LinkedIn of doctors" but is the moat as strong as it looks?

Executive summary

A highly profitable, asset-light platform. Doximity reaches over 80% of U.S. physicians and monetizes its verified network primarily through targeted pharmaceutical advertising, complemented by recruitment and workflow tools. The model delivers high gross margins, strong operating leverage, and substantial free cash flow.

Engagement driven more by utility than by network effects. While management emphasizes the social network as its moat, user behavior suggests physicians primarily use the platform for telehealth and workflow functionalities. This raises questions about the durability and depth of its competitive advantage.

Quality business, uncertain edge. Despite solid fundamentals and supportive industry tailwinds, competitive pressures (including AI-native entrants) and limited evidence of a strong moat make the investment case less clear-cut under a conservative return framework.

1. Business model

Doximity (DOCS 0.00%↑) is commonly known as the “LinkedIn for doctors”. The platform serves more than 3 million members, including >80% of U.S. physicians and >60% of U.S. nurse practitioners.

The business model combines a professional network with targeted marketing, recruitment solutions, and workflow tools.

Marketing Solutions: Marketing is the core economic engine. Doximity’s newsfeed appears to be the primary revenue contributor. According to the company, the platform reaches over 1 million unique active prescribers in a given quarter. Verified members can read medical articles, follow colleagues, and engage with professional content free of charge. Monetization occurs through targeted digital advertising sold primarily to biopharma companies. Doximity claims open rates are approximately 20x higher than those of Facebook or X, reflecting the platform’s focused audience and professional context.

Hiring Solutions: Doximity offers digital recruitment tools to hospitals and medical recruiting firms. The hiring product includes job postings and direct messaging functionality, both sold under annual subscription plans. The value proposition lies in direct access to a highly verified and concentrated physician base.

Workflow Solutions: Workflow products are designed to embed Doximity into daily clinical operations:

Dialer: Dialer allows physicians to call patients from their personal devices without exposing their private number. The free version allows one-to-one calls of up to 40 minutes. The Pro version is priced at $19.99 per user per month, with enterprise pricing available for larger organizations. Doximity also monetizes Dialer by displaying targeted advertisements before patients connect.

AI suite: DoxGPT is a physician-verified AI assistant designed to streamline administrative tasks such as summarizing faxes or drafting prior authorization letters. More recently, Doximity launched Doximity Scribe to support AI-powered note-taking. To our knowledge, these AI tools are not yet meaningfully monetized.

Scheduling tools: Doximity offers scheduling capabilities that enable physicians to coordinate patient appointments more efficiently, particularly within telehealth workflows. These tools integrate with Doximity Dialer and video services, allowing providers to send secure links to patients, manage virtual waiting rooms, and streamline appointment logistics.

e-Signature: Doximity provides secure electronic signature functionality tailored to healthcare use cases, such as signing clinical documents, consent forms, prior authorization paperwork, and administrative agreements. The tool is HIPAA-compliant.

Digital Fax: Digital Fax modernizes traditional fax workflows, which remain widely used in healthcare. Doximity enables physicians to send and receive faxes electronically through its platform, eliminating the need for physical fax machines. Incoming faxes can be digitized and integrated into electronic records, improving accessibility and reducing administrative burden.

2. Company history & ownership

Doximity was founded in 2010 by Jeff Tangney, Nate Gross, and Shari Buck. Tangney previously co-founded Epocrates, one of the earliest and most widely adopted mobile clinical reference tools for physicians. Epocrates provides clinicians with a drug reference database, including dosages, interactions, and contraindications.

In its early years, Doximity focused on creating a verified professional network exclusively for U.S. physicians. The company invested heavily in credential verification and offered free tools such as secure messaging and digital fax to drive adoption. Growth was largely organic, spreading through hospital systems and physician referrals. Early revenue came primarily from recruitment services, helping hospitals and healthcare systems hire doctors through targeted job listings.

As the network scaled, Doximity expanded into pharmaceutical marketing. By leveraging its verified physician database and specialty-level targeting capabilities, the company began offering highly precise digital advertising solutions to drug manufacturers.

Between 2017 and 2020, Doximity deepened its integration into physician workflows by launching tools such as Dialer and telehealth services. The COVID-19 pandemic significantly accelerated telehealth adoption, increasing physician engagement and reinforcing the platform’s utility beyond networking.

Doximity went public in June 2021 under the ticker DOCS. Although growth normalized after the pandemic surge, the company remains a dominant digital platform in the U.S. physician market, combining a professional network, workflow tools, and targeted healthcare marketing into a scalable business model.

In June 2025, OpenEvidence filed a lawsuit against Doximity, accusing the company of misappropriating trade secrets by allegedly impersonating physicians to gain access to its platform. The complaint claims that Doximity employees used the identities of real doctors to infiltrate OpenEvidence’s AI system and obtain confidential information. Doximity denied the allegations and, in September 2025, countersued OpenEvidence, asserting that the company had disseminated false and misleading statements and had harassed its employees.

2.2. Ownership

Doximity has a dual-class share structure with approximately 183 million shares outstanding as of January 29, 2026.

According to the latest proxy statement, Class A shares carry one vote per share, while Class B shares carry ten votes per share and are mostly owned by the CEO or affiliated parties (primarily the Family Trust). Jeffrey A. Tangney, co-founder and CEO, controls approximately 76% of the voting power while owning roughly 29% of the economic interest, which, in our opinion, ensures meaningful skin in the game.

It is also worth noting that Capital Group holds approximately 3% of the company.

3. Industry analysis

Doximity competes in two areas: social networking and marketing, hiring and workflow solutions:

Social Networking: Doximity competes against social behemoths like LinkedIn, Facebook, Google, or X. LinkedIn is a major platform for healthcare professionals with over 7.7M US members. In addition to the major social networks, there are other relevant though less known networks like Sermo. Sermo was founded in 2005 a social networking platform exclusive for physicians. Sermo claims to have >1.3M members which are also verified and derives revenue in the same way as Doximity.

Marketing, Hiring & Workflow Solutions: we regard Medscape as a very strong competitor in the pharma advertising market. Medscape was founded in 1995, enjoys strong brand recognition and i’ts also free to use with a global network of >6M users. The platform claims to reach 94% of all US physicians each month. Additionally, the company competes against a wide array of more or less specialized companies like audio/video (Zoom Video ZM 0.00%↑, American Well AMWL 0.00%↑, and Teladoc Health TDOC 0.00%↑ ), and organization tools (Microsft Teams or QGenda).

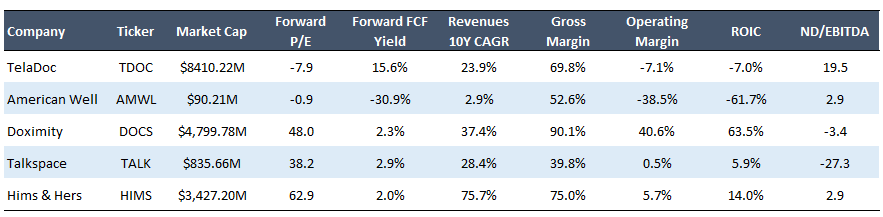

Doximity’s business is anchored in its physician network, which is not directly replicated by any publicly listed peer, making comparisons difficult. Teladoc and American Well focus primarily on telehealth infrastructure, whereas companies such as Talkspace and Hims & Hers provide medical services directly through the internet. Among these, we consider Teladoc the most relevant publicly traded peer.

4. Competitive advantage (moat)

The company identifies its social network and associated network effects as its primary competitive advantage. Undoubtedly, for a pharmaceutical company seeking digital access to U.S. physicians, Doximity is an important channel.

However, our research suggests that this moat may not be as strong as it appears.

After reviewing numerous user opinions online (Reddit, app stores, forums), we conclude that physicians primarily use the app for telehealth and workflow functionalities rather than for its social networking features.

Although users rate the app highly, the social feed does not appear to be the main driver of that satisfaction. If engagement is concentrated in utility features rather than network interaction, the strength of the network effect may be more limited than implied.

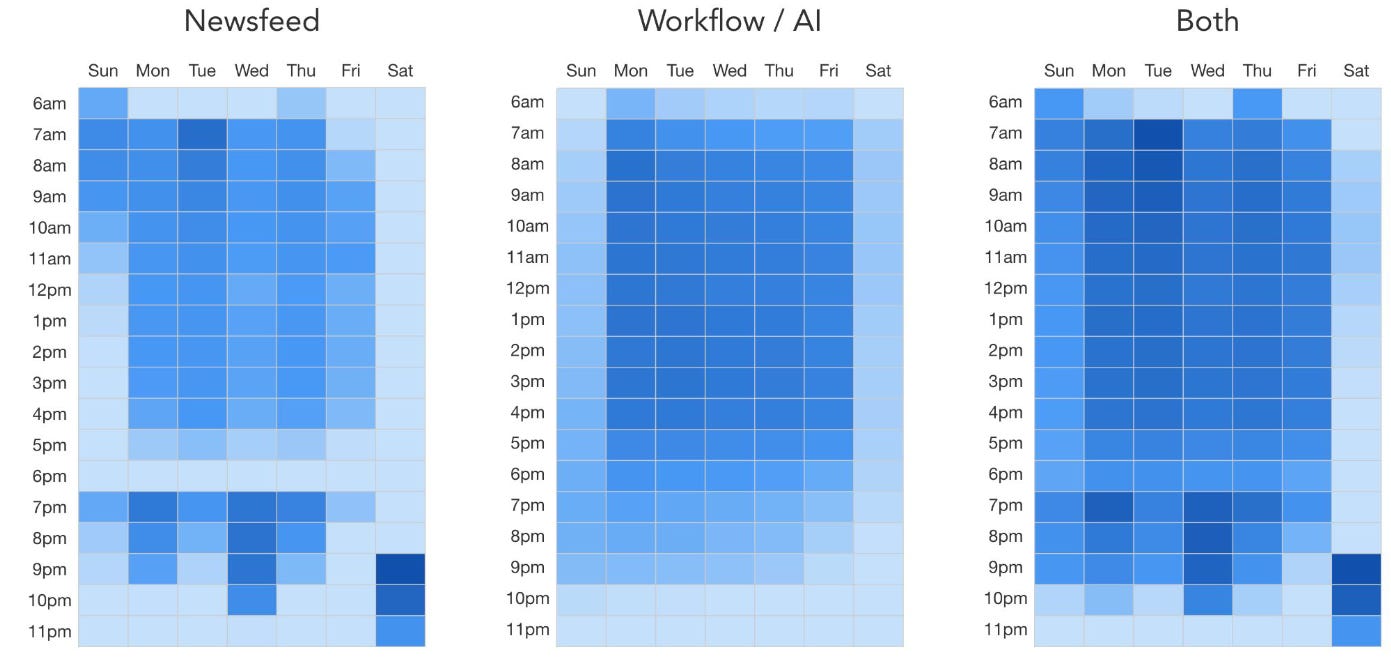

The company presents usage charts in its Winter 2026 Investor Presentation; however, these charts lack clarity. Darker shades represent “above-average usage” rather than absolute usage levels or growth. Moreover, it is unclear how “usage” is defined. For example, does one second of activity qualify as active use? These methodological questions are not sufficiently explained, limiting the conclusions that can be drawn.

Beyond the network, the competitive advantage of the company’s workflow tools (HIPAA-compliant communication, scheduling, Dialer, etc.) is also not entirely clear. While healthcare is a highly risk-averse industry (e.g., continued reliance on fax), we do not believe it would be particularly difficult for competitors to replicate these functionalities.

In our view, these tools do not appear deeply embedded or mission-critical to physician workflows in a way that would prevent disruption by new entrants.

Overall, based on publicly available information, we cannot confidently conclude that Doximity possesses a durable competitive advantage, and we lean toward the view that its moat may be limited or non-existent.

5. Financials

5.1. Growth & profitability:

The company was founded in 2010 and has grown rapidly since inception. COVID accelerated the adoption of digital tools within healthcare, although growth has since normalized. Nevertheless, the company continues to grow at a healthy pace.

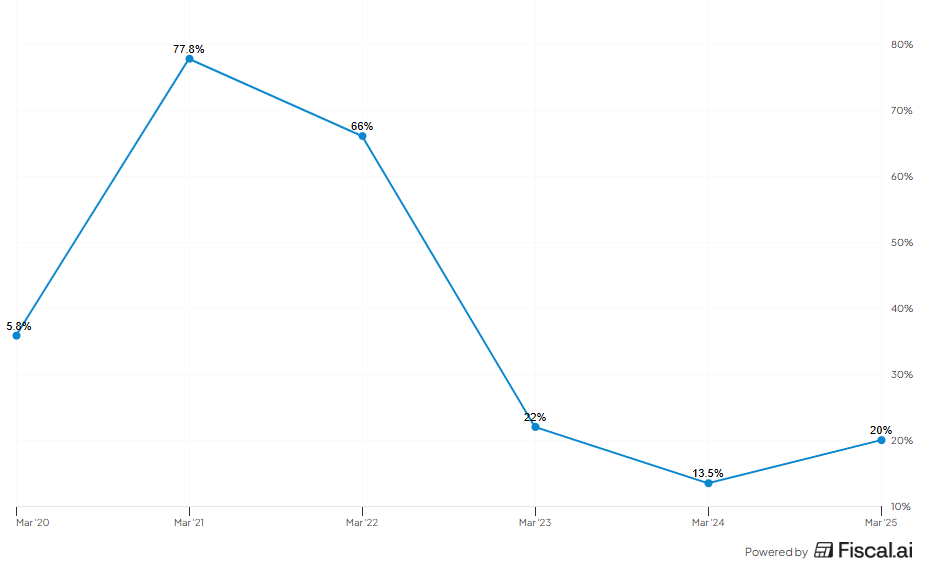

YoY Revenues Growth rate:

Management’s growth strategy follows a classic “land and expand” approach. Doximity prioritizes deepening relationships with existing clients through cross-selling and upselling opportunities. The pharmaceutical market opportunity remains significant, as the company continues to expand beyond existing brands and clients.

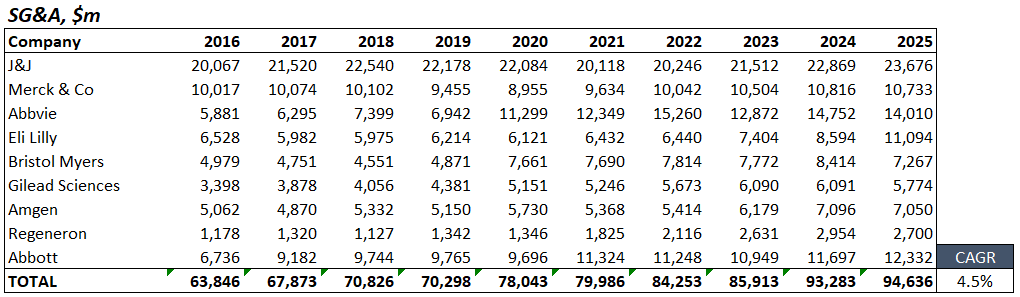

Demographic trends are supportive. As populations age, healthcare demand increases. We compiled SG&A expenses for the top 10 U.S. pharmaceutical companies, which have grown at a 4.5% CAGR since 2016. It is reasonable to expect digital marketing spending to grow at least in line with, if not faster than, overall SG&A.

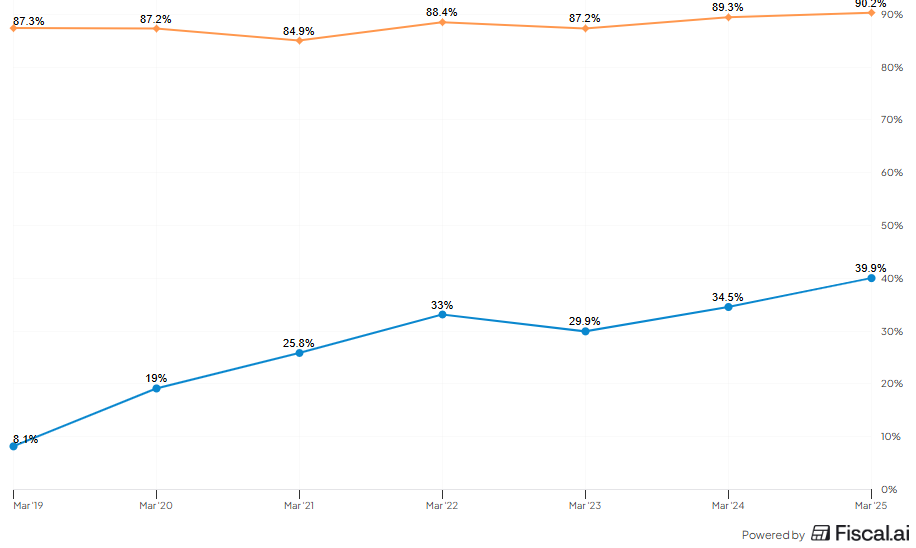

On the profitability side, operating margins have expanded due to operating leverage.

Gross margins (Orange line) and EBIT margin (Blue line):

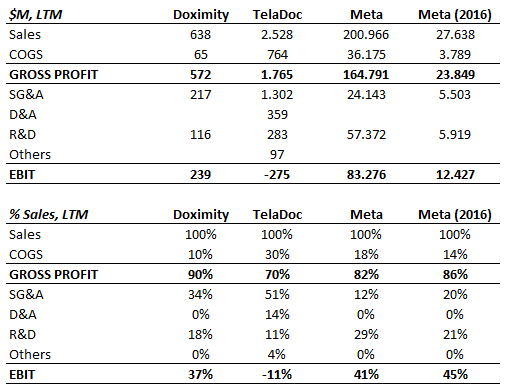

During our financial review, we noted the relatively low level of R&D investment for a growing technology company. When comparing major expense lines as a percentage of revenue (based on Fiscal.ai data), Doximity’s R&D intensity appears lower than Meta’s, despite Doximity operating at a significantly smaller scale. While this helps explain the company’s very high margin profile, margins at these levels warrant a degree of skepticism in our opinion. In competitive and innovation-driven markets — particularly with the rise of AI — sustained underinvestment in R&D could prove problematic over time. Although we cannot conclusively demonstrate that the company is underinvesting, the combination of unusually high margins and comparatively modest reinvestment raises questions about the long-term sustainability of current profitability.

5.2. Cash Flow generation and capital allocation:

The business model is inherently asset-light, resulting in strong free cash flow generation and high returns on invested capital.

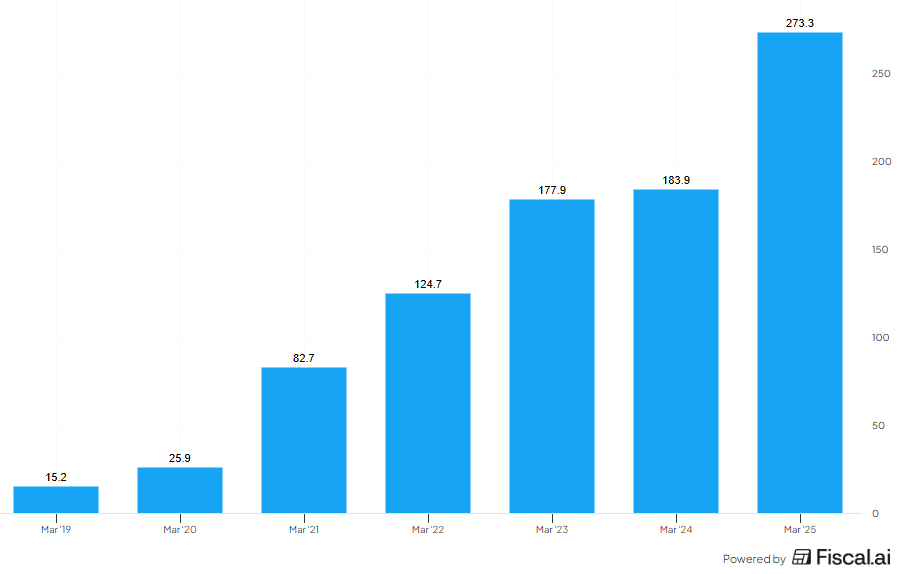

Evolution of FCF:

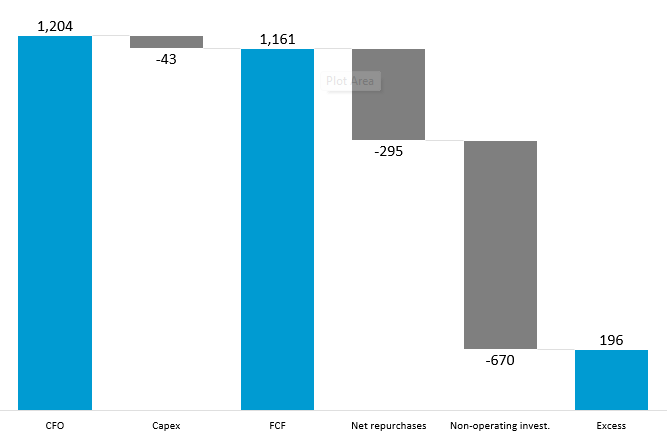

Accumulated cash flows over the last seven years provide further insight. Capital expenditures are minimal, as expected. The majority of generated cash has been retained within the company rather than distributed to shareholders which in our opinion is not the best option.

Accumulated Cash Flows (last 7 years):

5.3. Balance sheet and financial risk:

The company maintains a net cash position, taking into account its material holdings of marketable securities.

6. Valuation

We began analyzing the company after a recent sharp decline in the stock price.

Doximity had previously outlined long-term financial targets of reaching $1 billion in revenue by fiscal 2028, sustaining gross margins of 85–90%, and delivering EBITDA margins above 45%. The company later withdrew its revenue growth outlook, citing macroeconomic uncertainty.

Our valuation approach is intentionally simple. We prefer to choose the “easy questions of the exam” rather than looking for situations that are not clear to us. After two weeks reviewing the company, we conclude that either the business is not as strong as it initially appears, or we are unable to fully appreciate its strengths.

Nevertheless, we provide our framework.

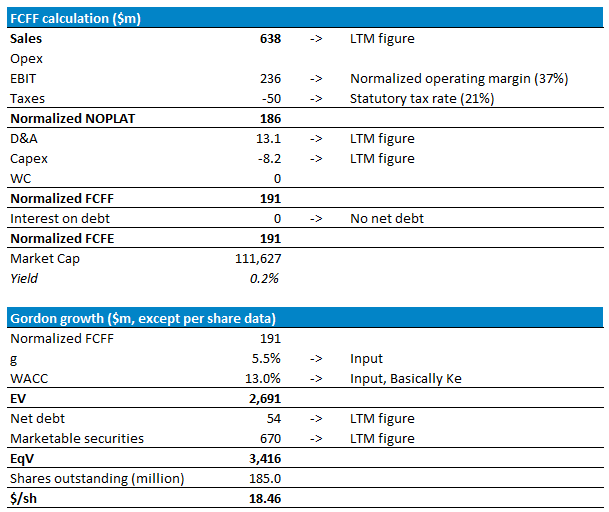

In a prior report on ADBE 0.00%↑ (link here), we applied a cost of equity of 11%, including a 100bps premium for AI-related and competitive risks. In this case, due to uncertainty around the business model, company size, and no/very thin moat, we apply a higher risk premium, resulting in a 13% cost of equity. As the company has no debt, WACC equals the cost of equity.

We assume long-term revenue growth of approximately 5.5%, reflecting 4.5% historical growth in pharma SG&A and incremental digital share gains, as well as continued client expansion and deeper penetration of existing accounts.

Disclaimer

As a reader of Black Tower Capital, you agree with our disclaimer. You can read the full disclaimer here.